The Department for Business, Innovation and Skills’ (BIS’s) free face-to-face advice for people struggling with debt has helped more people than planned, at slightly less than the planned cost per person, and is highly regarded by those that use it. However, demand is now outstripping capacity.

Jump to downloadsThe Department for Business, Innovation and Skills’ (BIS’s) free face-to-face advice for people struggling with debt has helped more people than planned, at slightly less than the planned cost per person, and is highly regarded by those that use it. However, demand is now outstripping capacity and support could be provided to more people through further efficiencies, the National Audit Office has reported. BIS also needs to engage more effectively with other parts of government working to help the over-indebted and with private sector advice providers.

UK consumers had £1,459 billion of outstanding debt at November 2009 and personal borrowing represented 160 per cent of household annual pre-tax income. While many people successfully manage their debt, research in 2008 by the Bank of England found that 11 per cent of people reported difficulty keeping up with their bills and credit commitments.

Since it began in April 2006, BIS’s face-to-face debt advice project has delivered help to some 270,000 people to the end of September 2009. An NAO survey found that 81 per cent of people who received the advice said it helped, compared to 69 per cent for advice received from a fee charging professional and 59 per cent for advice received from a bank.

In the recession, demand for support and advice has become greater than capacity. Between July 2008 and July 2009 there was a 28 per cent increase in the number of people contacting advice providers and, in some instances, there is not the capacity to cope. A quarter of advice agencies are either refusing new clients or have a waiting period of over a month.

BIS’s debt advice project is part of a government-wide strategy to support those struggling with debt. The strategy is complex with over 50 different projects, a number of funding streams, and diffuse responsibilities. Risks to value for money created by this complex delivery structure are not being controlled effectively by the current programme management arrangements. If the strategy is to succeed, there needs to be better governance, performance management and evaluation.

The NAO has also called for the Department to do more to evaluate how advice can be provided more efficiently, and to assess the role that all debt advice providers, including the private sector, could have in meeting Government’s aims for debt advice provision.

Findings

The Department for Business, Innovation and Skills’ (BIS’s) free face-to-face advice for people struggling with debt has helped more people than planned, at slightly less than the planned cost per person, and is highly regarded by those that use it. However, demand is now outstripping capacity and support could be provided to more people through further efficiencies, the National Audit Office has reported. BIS also needs to engage more effectively with other parts of government working to help the over-indebted and with private sector advice providers.

UK consumers had £1,459 billion of outstanding debt at November 2009 and personal borrowing represented 160 per cent of household annual pre-tax income. While many people successfully manage their debt, research in 2008 by the Bank of England found that 11 per cent of people reported difficulty keeping up with their bills and credit commitments.

Since it began in April 2006, BIS’s face-to-face debt advice project has delivered help to some 270,000 people to the end of September 2009. An NAO survey found that 81 per cent of people who received the advice said it helped, compared to 69 per cent for advice received from a fee charging professional and 59 per cent for advice received from a bank.

In the recession, demand for support and advice has become greater than capacity. Between July 2008 and July 2009 there was a 28 per cent increase in the number of people contacting advice providers and, in some instances, there is not the capacity to cope. A quarter of advice agencies are either refusing new clients or have a waiting period of over a month.

BIS’s debt advice project is part of a government-wide strategy to support those struggling with debt. The strategy is complex with over 50 different projects, a number of funding streams, and diffuse responsibilities. Risks to value for money created by this complex delivery structure are not being controlled effectively by the current programme management arrangements. If the strategy is to succeed, there needs to be better governance, performance management and evaluation.

The NAO has also called for the Department to do more to evaluate how advice can be provided more efficiently, and to assess the role that all debt advice providers, including the private sector, could have in meeting Government’s aims for debt advice provision.

Over-indebtedness

What is over-indebtedness?

While most consumers manage to service their personal debt, some cannot, especially at times of economic difficulty, and become over-indebted.

Over-indebtedness is ‘when consumers are unable to meet credit commitments from available income, taking account of minimal necessary expenditure’, according to research from University of Nottingham commissioned by BIS. This and other research into over-indebtedness is available from the BIS website.

Different groups of over-indebted consumers

The NAO’s work on over-indebtedness identified four distinct clusters within the over indebted population:

- Worried well: this group are not falling behind and do not have a high number of commitments, but sometimes struggle to keep up with repayments (49% of our sample).

- Worried and at risk: this group are currently keeping up, but they are always struggling to meet their repayments (14% of our sample).

- Over-Indebted: this group are not badly indebted, but are falling behind on a small number of bills (22% of our sample).

- Highly Over-Indebted: this group of consumers are the worst hit. They have the largest number of commitments, and are falling behind the most (15% of our sample).

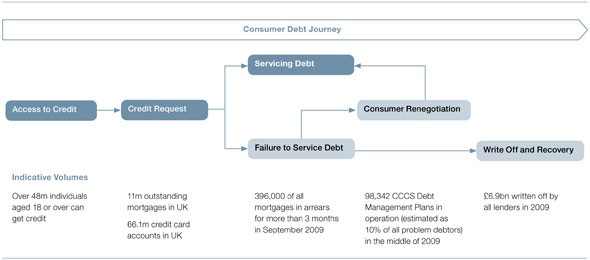

The consumer debt journey

A text description of the consumer debt journey (Word – 24KB) is available.

The problem

How big is the problem?

Over-indebtedness is difficult to measure. There is no nationally representative survey that measures people’s debts against their ability to pay, and it is difficult to identify how much money is needed to maintain a reasonable standard of living, because it will vary between individuals depending on a number of factors.

However, there are indicators of levels of debt, and of the numbers of consumers writing debt off:

- As at November 2009, consumers owed a total of £1,459bn, made up of £1,232bn of mortgage debt and £228bn of consumer debt – such as on credit and store cards

- In the second quarter of 2009, 33,073 people were granted a bankruptcy, Debt Relief Order or Individual Voluntary Arrangement. This was an increase of 27% on the same period in 2008

- Over 48 million people over 18 have access to credit

- There are 11 million outstanding mortgages in the UK

- There wee 61.1 million credit cards in the UK in 2009

- 396,000 mortgages were in reportable arrears at the end of the September 2009

For data and research on the scale of the problem as it changes, the following links may be of use:

Bank of England sources

The Bank of England provides a monthly release of growth rates, amounts outstanding and changes in total lending to individuals. This is broken down into both lending secured on dwellings and consumer credit.

The credit conditions survey asks bank and non-bank lenders about the past three months and the coming three months. It covers secured and unsecured lending to households and small businesses; and lending to non-financial corporations, and to non-bank financial firms.

The trends in lending survey provides data on aspects of lending to the UK corporate and household sectors.

Bank of England data set (LPQVTYC)

This data set provides an aggregate of total lending in the economy. It shows quarterly 12 month growth rate of total sterling net lending to individuals and housing associations (in percent seasonally adjusted). Data is available from 1963 to present day.

Other sources

The Insolvency Service provides statistics on insolvencies and court based debt solutions.

Social research providing data on individual household’s financial situation

The Wealth and Assets Survey provides information on the economic well-being of households and individuals in Great Britain. In particular the survey asks people about their assets and liabilities in order to estimate household and personal wealth.

Formerly known as the Survey of Low Income Families (SOLIF), the Families and Children Study (FACS) is a representative study of all families in Britain. It is a ‘true panel’ study, whereby 1999 respondents have been re-interviewed in subsequent annual waves from 2000 to 2004. It is designed to collect information about health, education, work, income, childcare and the wellbeing of children. In addition the FACS asks how households are getting on financially and therefore provides a picture of families’ debt situation.

The British home panel survey provides further understanding of social and economic change at the individual and household level in Britain to identify, model and forecast such changes, their causes and consequences in relation to a range of socio-economic variables.

Organisations with expertise in this area

The following organisations and centres of expertise have further information on consumer over-indebtedness.

The Personal Finance Research Centre at Bristol University

The Nottingham University Centre for Finance and Credit Markets

Case Studies

Case studies and other evidence

The National Audit Office carried out its own primary research on over-indebtedness. It includes:

- A survey of 1,361 consumers

- In depth interviews with 20 consumers

Read the data and findings from our research.

Where to find help with debt

The National Audit Office does not provide financial advice. Our audit included work with National Debtline, the Consumer Credit Counselling Service (CCCS), and Citizens Advice who might be able to help if you are worried about debt. We have included links to these organisations in the section below.

The list below is not intended to be comprehensive, and all the advice services we have spoken to have been facing increased demand for their services over the past year or so, so please be warned that there might be a delay before you can get an appointment or speak to someone on the phone. Free consumers advice is available from:

- National Debtline

- CCCS

- Citizens Advice

National Debtline

Website: http://www.nationaldebtline.co.uk

Telephone: 0808 808 4000

Opening Hours: 9.00 am to 9.00 pm Monday to Friday, 9.30am to 1.00 pm on Saturday

Email: email through the ‘contact us’ pages at http://www.nationaldebtline.co.uk/england_wales/contact_us.php

The Consumer Credit Counselling Service

Website: http://www.cccs.co.uk

Telephone: 0800 138 1111

Opening hours: 8am to 8pm Monday to Friday

Citizens Advice

Website: http://www.citizensadvice.org.uk

"Many people are able to manage their debt, but for some the problems may seem insurmountable. When that is the case, people need good advice which they can trust and which is accessible. BIS’s project to offer face-to-face advice has done well and has helped those who have used it. But demand is outstripping capacity and the Department needs to look at ways of reaching even more people; and it must establish a coherent framework for delivering the Government’s wider strategy for tackling over-indebtedness."

Amyas Morse, head of the National Audit Office

Downloads

- 0910292.pdf (.pdf — 279 KB)

- 0910292es.pdf (.pdf — 68 KB)

- debt_analytical_supplement.pdf (.pdf — 128 KB)

- n0910292_methodology.pdf (.pdf — 71 KB)

- consumer_debt_journey.doc (.msword — 24 KB)

Publication details

- ISBN: 9780102963458 [Buy a hard copy of this report]

- HC: 292, 2009-10